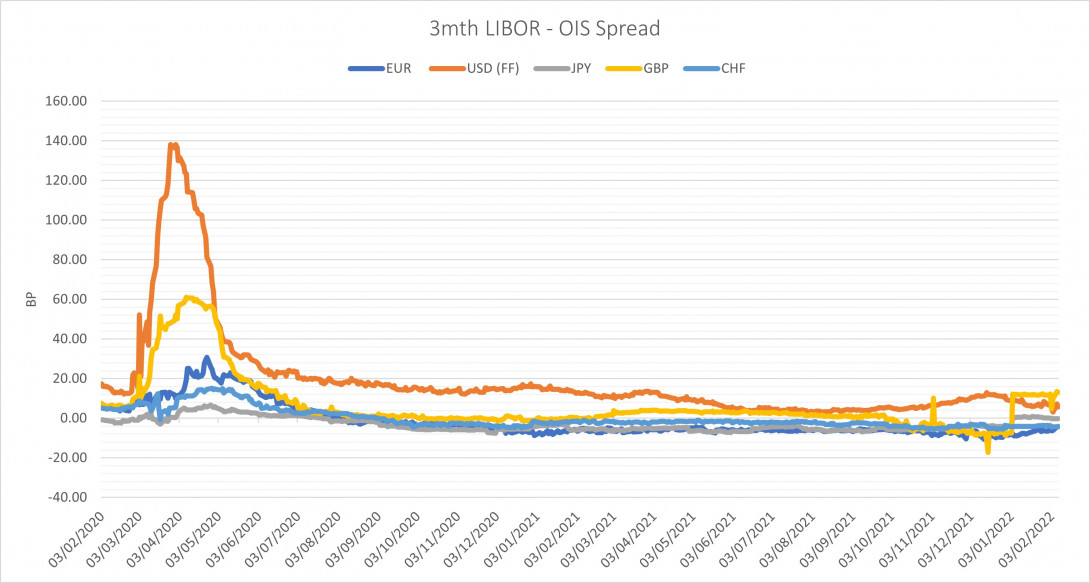

The spread between the 3mth London Interbank Offered Rate (LIBOR) or equivalent and the overnight index swap (OIS) - often referred to as the ‘LOIS’ – is used as a barometer of money market stress, indicating the disparity between secured and unsecured short-term funding.

Source: ICMA analysis using Bloomberg data (February 2022)